A kitchen fire that forces you to close for two weeks. A customer who slips on a wet floor and sues for $300,000. An employee who cuts their hand on a mandoline and needs surgery. These are not hypotheticals — they are the kinds of events that end restaurants that were not properly insured. According to Cuisine Coverage’s 2025 data on restaurant insurance, a surprising 38% of U.S. restaurant owners lacked adequate business insurance coverage in 2025, up from 29% the year prior. In a city as expensive and litigious as New York, running without proper insurance is a bet that most operators cannot afford to lose. This guide breaks down exactly which policies you need, which are legally required in New York State, and how to avoid paying for coverage you do not actually need.

Key Takeaways

- Workers’ compensation insurance is legally required by New York State for any business with employees — no exceptions for restaurants.

- General liability insurance is not legally mandated by the state, but most commercial landlords in NYC require it as a condition of your lease.

- If you serve alcohol, liquor liability insurance is essential — New York courts routinely hold restaurants liable for damages caused by intoxicated patrons.

- A Business Owner’s Policy (BOP) bundles general liability, property, and business interruption into one cost-effective package suited for most small restaurants.

- Business interruption insurance is the coverage most restaurant owners discover they needed only after a closure forces them to pay rent and payroll with no revenue coming in.

Legally Required Insurance in New York State

Workers’ Compensation Insurance

New York State law requires every employer — including restaurants with even a single employee — to carry workers’ compensation insurance. There are no exceptions for small businesses or part-time workforces. Workers’ comp covers medical expenses, rehabilitation costs, and wage replacement for employees injured on the job. For restaurants, this matters enormously: kitchens are hazardous environments where burns, knife cuts, slip-and-fall injuries on wet floors, and musculoskeletal injuries from heavy lifting are a daily reality. According to Hi Bluerock’s guide to NYC restaurant insurance, workers’ comp is not optional — it is mandatory by New York law, and failing to carry it exposes you to both state fines and personal liability if an employee is injured while uninsured.

Workers’ comp premiums are calculated based on payroll and job classification. Restaurant kitchen workers carry a higher classification risk — and thus higher premiums — than administrative staff. Make sure your employees are classified correctly to avoid both overpaying and being underinsured.

Disability Benefits Insurance

New York State also requires most private employers to provide disability benefits coverage for off-the-job illness or injury that leaves an employee unable to work. This is separate from workers’ comp (which covers on-the-job injuries) and is often overlooked by restaurant owners. It can be purchased through the New York State Insurance Fund or a private carrier.

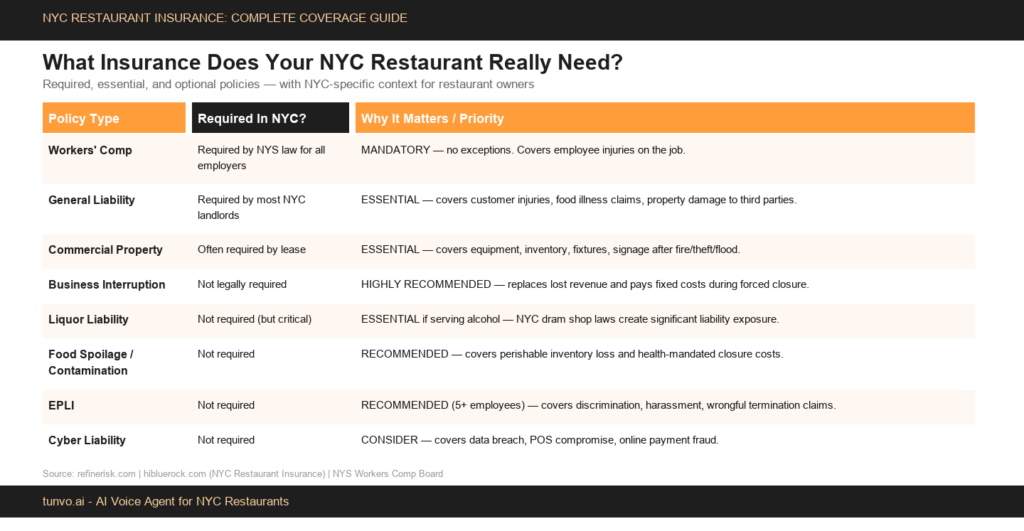

Essential Policies Every NYC Restaurant Needs

NYC restaurant insurance at a glance: what is required, what is essential, and what to consider based on your operation.

NYC restaurant insurance at a glance: what is required, what is essential, and what to consider based on your operation.General Liability Insurance

General liability insurance is the foundational coverage for any restaurant — protecting your business against third-party claims of bodily injury, property damage, and personal injury. In NYC, this is the policy that activates when a customer slips and falls in your dining room, claims food poisoning after eating your food, or suffers a burn from spilled hot liquid. It covers legal defense costs, medical payments to injured parties, and settlement costs. As noted by Refine Risk’s guide to NYC restaurant insurance, most commercial landlords require proof of general liability insurance — typically $1 million per occurrence — before signing a lease or renewing one. Without it, you cannot legally operate in most NYC commercial spaces.

General liability for a small-to-midsize NYC restaurant typically runs between $500–$2,000 per year depending on the size of your space, annual revenue, and claims history. Some Business Owner’s Policies (BOPs) bundle general liability with property coverage at a discount, making a BOP more cost-effective than purchasing coverage separately.

Commercial Property Insurance

Commercial property insurance protects the physical assets of your restaurant: kitchen equipment, furniture, fixtures, inventory, signage, and the building if you own it. In New York City, where restaurant buildouts cost hundreds of thousands of dollars, replacing commercial kitchen equipment after a fire or flood without insurance is a business-ending event for most operators. Property coverage pays to repair or replace damaged assets after covered events — typically fire, theft, vandalism, burst pipes, and some weather events.

If you lease your space, your lease almost certainly requires you to carry property insurance covering your improvements and equipment. Your landlord’s building insurance covers the structure itself, but it does not cover what you brought inside or what you installed. Read your lease carefully to understand what you are required to insure.

Business Interruption Insurance

Business interruption insurance — also called business income insurance — replaces lost revenue and covers ongoing fixed expenses (rent, loan payments, payroll) when a covered event forces you to close temporarily. It is the coverage most restaurant owners wish they had purchased before they needed it. According to Refine Risk’s NYC restaurant coverage guide, some Business Owner’s Policies include business interruption coverage built-in, though coverage limits and waiting periods vary significantly by policy. Review your policy’s “restoration period” — this is how long the insurer will pay out after a covered closure. For a kitchen fire that takes three months to repair, you need a restoration period of at least 90 days.

Business interruption insurance is typically triggered by the same events as your property insurance — fire, certain weather events, equipment failures. Notably, most standard policies did not cover COVID-related closures (a lesson the restaurant industry learned painfully in 2020). Some carriers now offer pandemic or government-mandated-closure endorsements, though pricing varies considerably.

If You Serve Alcohol: Liquor Liability Is Non-Negotiable

New York has strict dram shop laws that hold establishments liable for damages caused by patrons who were served alcohol while visibly intoxicated. If a customer drinks at your restaurant, drives, and causes an accident that injures or kills someone, your restaurant can be sued. Standard general liability policies explicitly exclude alcohol-related claims. You need a standalone liquor liability policy or a dram shop endorsement added to your existing coverage. As Refine Risk’s guide notes, NYC courts frequently rule in favor of injured third parties in alcohol-related cases, and judgments can be substantial. If your restaurant does any alcohol service at all — wine with dinner, beer with takeout — liquor liability insurance belongs in your portfolio.

Additional Coverage Worth Considering

Food Contamination and Spoilage Insurance

If your walk-in cooler fails overnight or a power outage spoils your seafood inventory, food spoilage insurance covers the cost of replacing perishable inventory. This is often added as an endorsement to your commercial property policy at relatively low cost. For restaurants with high-value perishable inventory — fresh fish, live shellfish, aged meats, specialty produce — even a single equipment failure without this coverage can cost thousands of dollars in spoiled product alone. Food contamination coverage extends further, covering cleanup costs if your kitchen is found to be contaminated and loss of business income during a health-mandated closure.

Employment Practices Liability Insurance (EPLI)

EPLI protects your restaurant against claims from employees alleging discrimination, harassment, wrongful termination, or retaliation. Restaurant environments — with close working conditions, high turnover, and sometimes blurry personal/professional boundaries — generate a disproportionately high number of EPLI claims. In NYC, where employment law provides broad worker protections and the legal culture is plaintiff-friendly, EPLI is increasingly viewed as essential rather than optional for any restaurant with more than a handful of employees.

Cyber Liability Insurance

If your restaurant accepts credit cards, uses a POS system connected to the internet, or collects customer data through an online ordering system, you have cyber exposure. A data breach that exposes customer payment information can trigger notification obligations, regulatory fines, and customer claims. Cyber liability insurance covers breach response costs, legal fees, and regulatory penalties. As Insurance Resource NY’s guide to restaurant coverage notes, cyber attacks on small businesses are increasingly common, and the costs of a breach without insurance can be devastating for a restaurant without large cash reserves.

Bundling with a Business Owner’s Policy (BOP)

For most independent NYC restaurants, a Business Owner’s Policy (BOP) is the most cost-effective way to purchase core coverage. A BOP bundles general liability, commercial property, and business interruption insurance into a single policy. According to Rezku’s 2025 restaurant insurance guide, BOPs are typically priced lower than purchasing each component separately because insurers price the bundle efficiently. Many restaurant-specific BOPs can also be extended with endorsements for liquor liability, food spoilage, or EPLI, creating a nearly comprehensive program under one policy.

| Policy | Required? | Est. Annual Cost (NYC) | Priority |

|---|---|---|---|

| Workers’ Compensation | Yes (NYS law) | Varies by payroll | Mandatory |

| General Liability | Required by most landlords | $500–$2,000/yr | Essential |

| Commercial Property | Often required by lease | $1,000–$4,000/yr | Essential |

| Business Interruption | Not required | Often bundled in BOP | Highly Recommended |

| Liquor Liability | Not required (but critical if you serve alcohol) | $500–$2,500/yr | Essential if serving alcohol |

| Food Spoilage / Contamination | Not required | $200–$500/yr add-on | Recommended |

| EPLI | Not required | $500–$2,000/yr | Recommended (5+ employees) |

| Cyber Liability | Not required | $500–$1,500/yr | Consider if using POS/online ordering |

How to Buy Restaurant Insurance in NYC

Work with a Commercial Insurance Broker

Do not rely solely on online quote comparison tools for restaurant insurance. Restaurant operations have specific exposures — food service equipment, open flames, alcohol service, high foot traffic — that require an agent experienced with the hospitality industry to underwrite accurately. A commercial broker who specializes in restaurants can identify gaps in coverage, negotiate better terms with carriers, and ensure your policy documents say what you think they say. Ask specifically for the restaurant or food service specialty within their practice, not a generalist who occasionally insures restaurants.

Review Your Lease Before Buying Coverage

Read your commercial lease for insurance requirements before purchasing any policy. Most NYC commercial leases specify minimum coverage amounts (commonly $1 million per occurrence for general liability, $2 million aggregate), require that the landlord be named as an “additional insured,” and specify what types of property you are required to insure. Buying a policy that does not meet your lease terms — even if it is otherwise adequate — can expose you to lease violations and potential eviction.

Reassess Coverage After Major Changes

Your insurance needs change as your restaurant changes. If you add a bar or beer/wine service, you need liquor liability. If you add a delivery fleet, you need commercial auto. If you expand your kitchen equipment, your property coverage limit may need to increase. Review your policies annually — or whenever you make a significant change to your operation — and inform your broker of what has changed.

At Tunvo, we talk to NYC restaurant owners every day about what it takes to run a sustainable operation. Insurance is the foundation that lets you take risks — launching a new menu, hiring more staff, taking on a second location — without risking everything you have built. Learn more about Tunvo’s approach to supporting NYC restaurants, from operational tools to the conversations we have with owners about running smarter businesses.

Frequently Asked Questions

Is general liability insurance required by law in New York State?

New York State does not legally mandate general liability insurance for restaurants as a condition of operating. However, it is effectively required because: (1) most commercial landlords require it as a condition of signing or renewing a lease, and (2) operating a food service business without it exposes you to unlimited personal liability for customer injuries, property damage, and food illness claims. In practice, no NYC restaurant should operate without it.

What does a Business Owner’s Policy (BOP) cover?

A BOP typically bundles general liability, commercial property, and business interruption insurance into a single policy at a lower combined cost than purchasing each separately. It provides foundational coverage for most small-to-midsize restaurants. You can add endorsements for liquor liability, food spoilage, EPLI, and other specific risks to customize the coverage to your operation.

Do I need insurance if I only have two or three employees?

Yes. New York State workers’ compensation law applies to all private-sector employers with any employees — there is no minimum headcount exemption. Even if your restaurant has one full-time employee and one part-time employee, you are legally required to carry workers’ compensation insurance.

How much does restaurant insurance typically cost in NYC?

Total insurance costs for a small-to-midsize NYC restaurant typically range from $5,000–$20,000 per year in total premiums across all policies, depending on the size of your operation, annual revenue, whether you serve alcohol, and your claims history. A BOP for a small restaurant without alcohol service might run $2,000–$5,000/year. Workers’ comp adds additional cost based on your payroll. The specific premium depends heavily on your individual risk profile — get quotes from at least two or three specialized restaurant insurance brokers before deciding.

Does my general liability policy cover food poisoning claims?

Most general liability policies include “products liability” coverage, which covers claims arising from food you served — including food poisoning. However, policy wording varies. Make sure your policy explicitly includes products and completed operations liability, and check any exclusions that might apply to contamination or foodborne illness claims. If you have concerns, discuss this specifically with your broker.

The best protection is prevention — and so is capturing every opportunity. Proper insurance protects your restaurant when things go wrong. Tunvo’s AI voice agent ensures nothing goes wrong with your phone orders — every call is answered, every order is captured, and your staff can focus on the floor. According to Tunvo, restaurants using AI voice ordering see 13%+ higher order revenue by eliminating missed calls during peak hours. Book a free demo and see what it can do for your restaurant.